(Bloomberg) -- Mario Draghi’s reign as European Central Bank president is ending much like that of his predecessor -- with a plea for fiscal coordination to fix a monetary union that is incomplete without it.

The outgoing chief singled out the creation of a mechanism to harness the region’s collective budget resources as the key element missing in the design of the common currency. That’s reminiscent of the outgoing Jean-Claude Trichet’s call in 2011 for a revamp of economic governance of the euro amounting to a “quantum leap” -- envisaging an eventual “ministry of finance of the union.”

The euro zone is unusual in that the bloc’s 19 countries share a single currency but keep national control of their own budgets.

“There is one thing that all the successful monetary unions have, and that’s a central fiscal capacity -- in other words, whether this should be a budget or should be a system of insurance,” Draghi told reporters at his final press conference in Frankfurt on Thursday.

The insights of both ECB chiefs illustrate how, despite the existential debt crisis that afflicted the currency during both their terms, progress in deepening economic integration has been slow beyond the notable exception of establishing a common banking supervisor. A euro-zone budget is now in the making, but might still not amount to much.

“Draghi is right that probably a central fiscal authority has much better chances to act where there are weaknesses, but also in injecting more confidence,” said Anatoli Annenkov, an economist at Societe Generale (PA:SOGN). “The problem of course is more political. If we get more fiscal union, we probably need more political integration.”

Moral Hazard

A key challenge is that fiscal hardliners such as Germany and the Netherlands are wary of sharing liabilities with indebted countries such as Italy and Greece. Draghi acknowledged their concerns, saying the architecture of any common budget tool was crucial.

“This should be designed in a way that doesn’t create moral hazard,” he said. “I think that’s one of the main reasons for the slow progress on that front, is the risk that the mechanisms would be used for increasing moral hazard.”

Euro-area finance ministers agreed this month on elements of a small budget for the currency bloc that falls far short of the original sweeping vision of French President Emmanuel Macron, who has pushed the initiative. Talks on financing the measure have been delayed.

Draghi alluded to the need for any such tool to be big enough to have an effect.

“It’s very important to have something of that nature, of an adequate size. Something that can be used counter-cyclically, something that would basically take care of the fact that national fiscal policies have, in my view, limited spillovers on the rest of the euro zone.”

Convincing countries with budget space to deploy it to aid economic growth as a complement to monetary policy is a priority for the ECB now. Draghi said last month that it’s “high time for the fiscal policy to take charge,” and reiterated that sentiment in his opening statement, agreed with his colleagues.

“The ECB has always reacted quite preemptively or proactively and their wish is probably for fiscal policy to react in the same way,” said Annenkov.

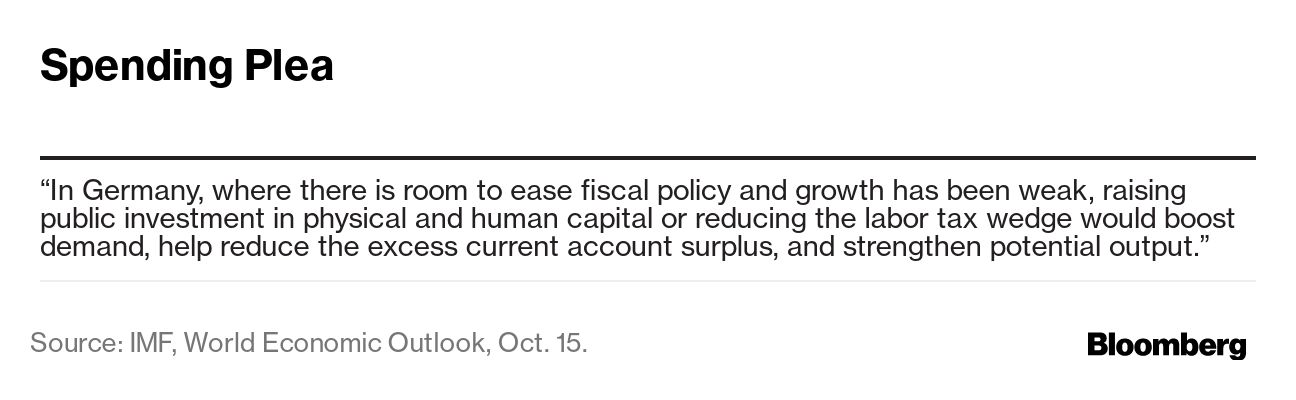

The most important candidate that could help out is Germany, the euro zone’s biggest economy and most populous member, which has kept borrowings low by following a path of fiscal prudence that avoids deficits. Last week, the International Monetary Fund called for the country to ramp up investment.

While Draghi’s references to countries with “fiscal space” clearly include Germany, he’s typically careful to avoid naming specific governments, which would draw accusations of crossing the line that supposedly separates monetary and fiscal policy.

On Thursday, invited to comment on Germany’s constitutional debt brake, which limits the extent of any stimulus it might add, he shirked from a direct comment.

“I can’t answer,” he said. “I would never dare to judge fiscal policies in one specific country.”