- CPI inflation data, start of Q4 earnings season in focus.

- Delta Air Lines shares are a buy with upbeat earnings on deck.

- Macy’s stock set to struggle after warning of soft holiday sales.

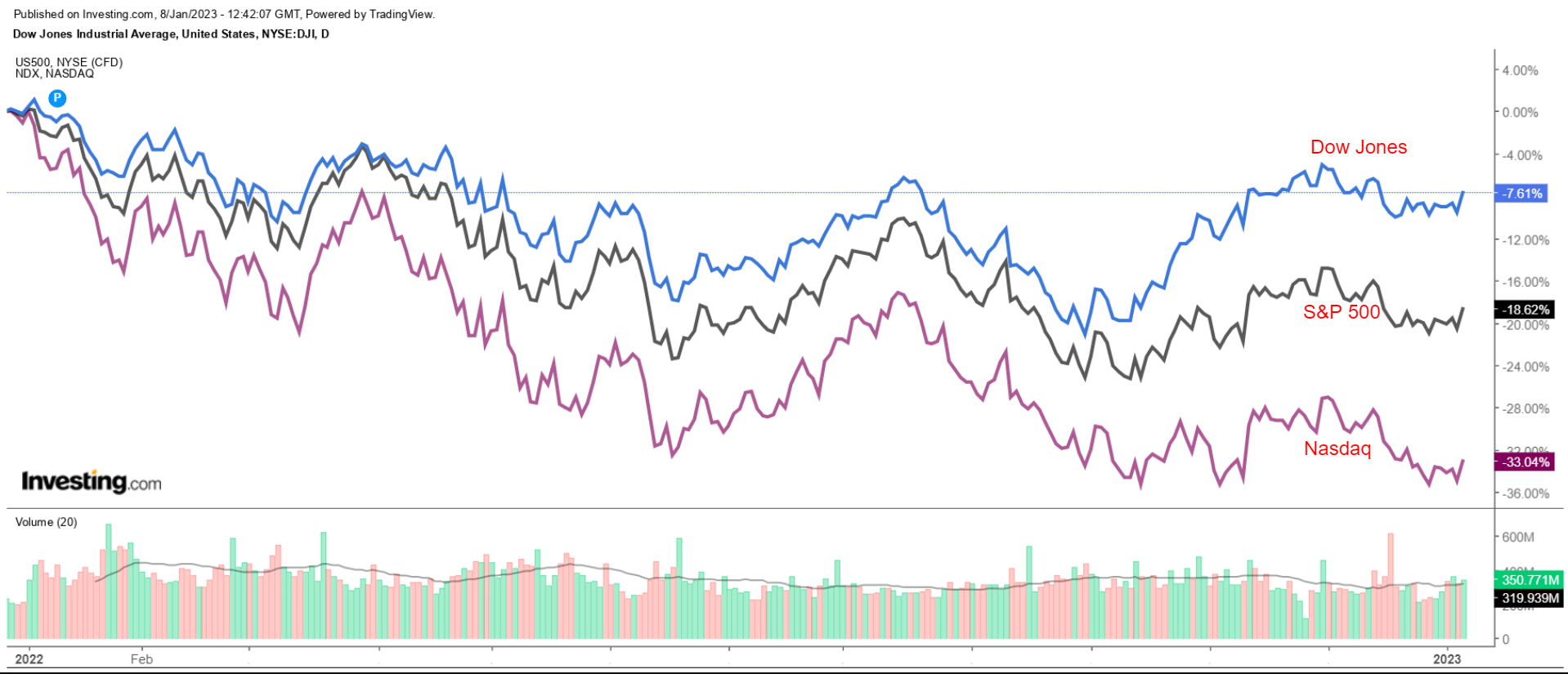

Stocks on Wall Street soared on Friday, with the major indices all gaining more than 2% as investors bet that the Federal Reserve may not become as aggressive as some had feared after the December jobs report showed signs that inflation may be cooling.

For the holiday-shortened week, the blue-chip Dow Jones Industrial Average rose 1.5%, while the benchmark S&P 500 and technology-heavy Nasdaq Composite advanced 1.4% and 1% respectively to snap four weeks of declines.

Source: Investing.com

The week ahead is expected to be a busy one, as investors brace for the first full trading week of 2023.

On the economic calendar, most important will be Thursday’s U.S. consumer price inflation report for December, which is forecast to show headline annual CPI cooling to 6.5% from the 7.1% increase seen in November.

A lower-than-expected CPI reading could seal the deal for a Fed downshift to a 25-basis-point rate hike at next month’s policy meeting.

Meanwhile, the earnings season officially kicks off on Friday with JPMorgan Chase (NYSE:JPM), Bank of America (NYSE:BAC), Citigroup (NYSE:C), and Wells Fargo (NYSE:WFC) all scheduled to release quarterly results.

Regardless of which direction the market goes, below we highlight one stock likely to be in demand and another that could see further downside.

Remember, though, our time frame is just for the week ahead.

Stock To Buy: Delta Air Lines

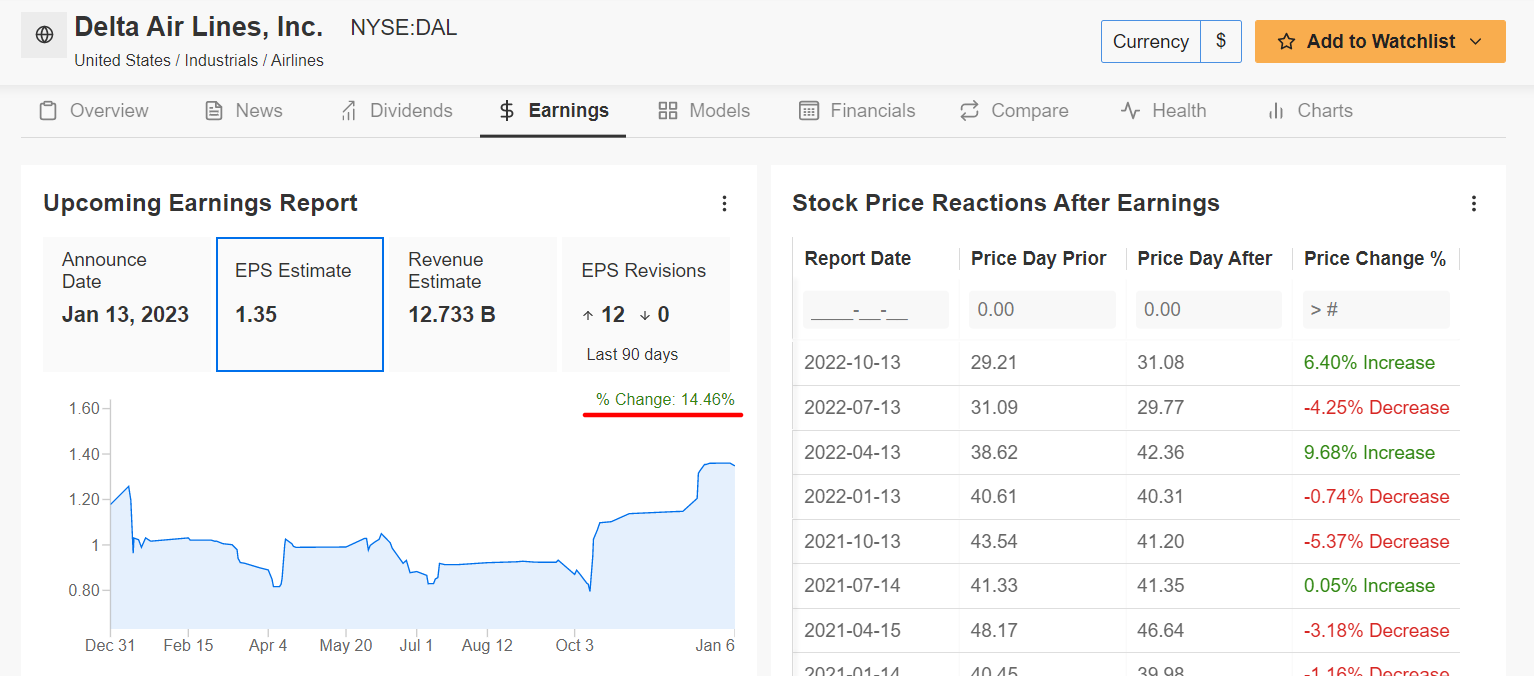

After closing at their best level since June on Friday, I expect shares of Delta Air Lines (NYSE:DAL) to continue their rally in the coming week as the legacy carrier is forecast to deliver upbeat profit and sales growth when it reports its latest financial results ahead of the open on Friday, Jan. 13.

As per moves in the options market, traders are pricing in a significant swing of around 5.3% in either direction for DAL stock following the earnings update.

An InvestingPro survey of analyst earnings revisions points to mounting optimism ahead of Delta's report, with analysts raising their EPS estimates 12 times over the last 90 days to reflect an increase of roughly 14.5% from their initial expectations.

Source: InvestingPro+

Consensus estimates call for the Atlanta-based company to post fourth-quarter earnings per share of $1.35, up over 500% from EPS of just $0.22 in the year-ago period, as profitability trends continue to recover from the COVID-19 pandemic. Meanwhile, revenue is forecast to accelerate 34.4% year over year to $12.73 billion amid the ongoing improvement in air travel demand.

In my opinion, Delta’s results will easily surpass expectations thanks to robust domestic demand for both leisure and corporate travel while benefitting from increasing international traffic after the company reopened routes to key destinations in Europe and China.

As a result, I believe Delta’s management will provide strong sales guidance for the first three months of the new year, as the carrier remains well placed to thrive despite a difficult backdrop of rising interest rates, elevated inflation, and slowing economic growth.

In my view, the company - which was named North America's most on-time airline for 2022 - will be the main beneficiary from the debacle surrounding Southwest's (NYSE:LUV) flight delays during the Christmas blizzard of 2022 due to Delta's reputation for greater reliability during peak travel times.

Source: Investing.com

DAL stock ended at $36.03 on Friday, its highest close since June 9, 2022. At current levels, Delta has a market cap of over $23 billion, earning it the status of the world’s most valuable airline company.

Shares, which have bounced off their October lows along with the major stock indices, soared 9.6% in the first trading week of 2023 after suffering an annual loss of 15.9% in 2022.

Stock To Dump: Macy’s

I anticipate Macy’s (NYSE:M) stock will suffer a challenging week ahead as investors react to fresh negative developments plaguing the world’s largest department-store chain.

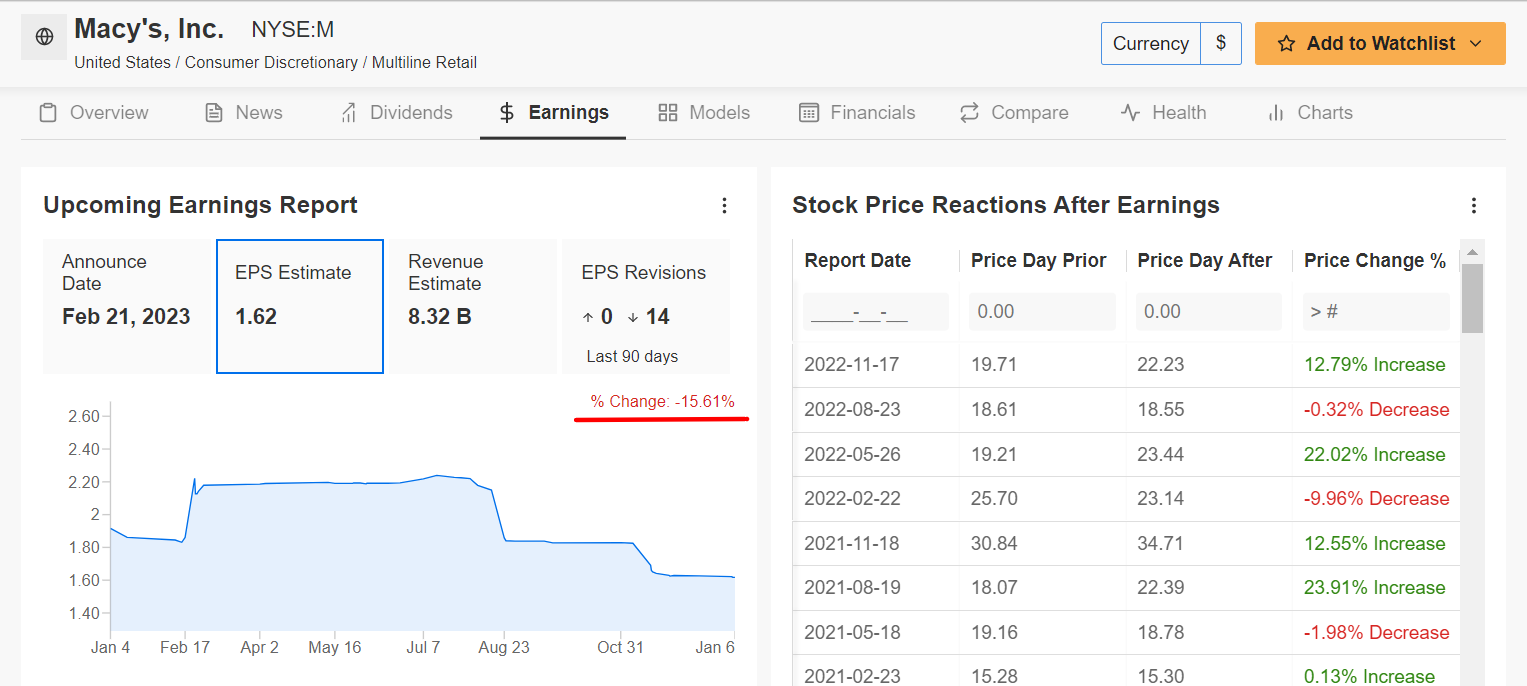

Macy’s warned on Friday that it expects fourth-quarter sales to come in at the lower end of its forecast, blaming a deeper-than-expected lull in shopping during the non-peak holiday weeks between Black Friday and Christmas.

The retailer also cautioned that consumer spending would remain under pressure in 2023, especially in the first half.

Macy’s net sales for the holiday quarter are now expected to be at the low-end to midpoint of its previously issued range of $8.16 billion to $8.40 billion.

Like many other major U.S. retail names, Macy’s has been struggling due to a combination of several macro and fundamental headwinds, such as higher interest rates, mounting inflationary pressures, slowing growth, and lingering inventory and supply-chain woes.

Source: InvestingPro+

Macy’s is tentatively scheduled to report Q4 financial results ahead of the U.S. market open on Tuesday, Feb. 21.

Consensus calls for earnings per share of $1.62, falling 33.9% from EPS of $2.45 in the year-ago period due to the negative impact of rising operating expenses, higher cost pressures and declining operating margins.

Going into the report, EPS estimates have been revised downward 14 times in the past 90 days, to indicate a -15.6% drop from initial expectations.

Revenue meanwhile is forecast to decline 4.1% y-o-y to $8.32 billion, as shoppers cut back spending on luxury fashion items amid the current inflationary environment, which is causing disposable income to shrink.

Source: Investing.com

M stock ended Friday’s session at $22.13, earning the New York-based company a market valuation of $6 billion. Shares jumped roughly 7.2% to start off 2023 after falling 21.1% last year.

Disclosure: At the time of writing, I am short on the S&P 500 and Nasdaq 100 via the ProShares Short S&P 500 ETF (NYSE:SH) and ProShares Short QQQ ETF (NYSE:PSQ). I remain long on the Energy Select Sector SPDR ETF (NYSE:XLE) and the Health Care Select Sector SPDR ETF (NYSE:XLV).

The views discussed in this article are solely the opinion of the author and should not be taken as investment advice.

***

The current market makes it harder than ever to make the right decisions. Think about the challenges:

- Inflation

- Geopolitical turmoil

- Disruptive technologies

- Interest rate hikes

To handle them, you need good data, effective tools to sort through the data, and insights into what it all means. You need to take emotion out of investing and focus on the fundamentals.

For that, there’s InvestingPro+, with all the professional data and tools you need to make better investing decisions. Learn More »

Which stock should you buy in your very next trade?

With valuations skyrocketing in 2024, many investors are uneasy putting more money into stocks. Unsure where to invest next? Get access to our proven portfolios and discover high-potential opportunities.

In 2024 alone, ProPicks AI identified 2 stocks that surged over 150%, 4 additional stocks that leaped over 30%, and 3 more that climbed over 25%. That's an impressive track record.

With portfolios tailored for Dow stocks, S&P stocks, Tech stocks, and Mid Cap stocks, you can explore various wealth-building strategies.