- U.S. retail sales, housing data, more earnings in focus

- Chevron stock is a buy amid ongoing energy sector rally

- Target shares set to struggle amid weak Q3 profit, sales

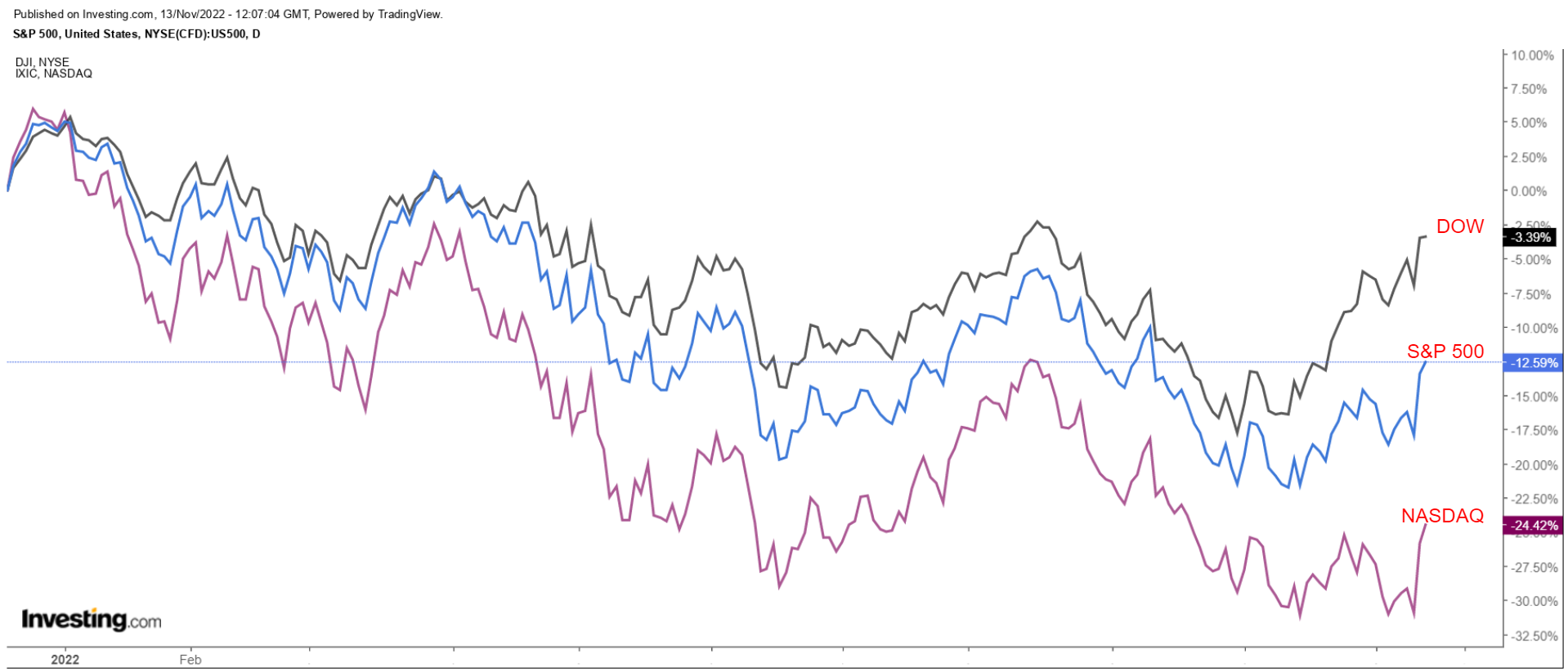

Stocks on Wall Street rallied on Friday to notch their biggest weekly gain since June as investors cheered signs that inflation may be peaking, raising hopes the Federal Reserve will be less aggressive on interest rate hikes.

For the week, the blue-chip Dow Jones Industrial Average rose 4.1%, while the benchmark S&P 500 and technology-heavy Nasdaq Composite jumped 5.9% and 8.1%, respectively.

The S&P 500 is now up 14.3% from a mid-October low, however it remains about 16% lower for the year, on course for its biggest annual decline since 2008.

Source: Investing.com

The week ahead is expected to be another busy one amid more earnings from notable companies like Walmart (NYSE:WMT), Home Depot (NYSE:HD), Lowe’s (NYSE:LOW), Macy’s (NYSE:M), Kohls Corp (NYSE:KSS), TJX (NYSE:TJX), Nvidia (NASDAQ:NVDA), Cisco (NASDAQ:CSCO), Alibaba (NYSE:BABA), JD.com (NASDAQ:JD), Tencent (OTC:TCEHY), and ZIM Integrated Shipping (NYSE:ZIM).

In addition to earnings, retail sales and housing data (building permits, housing starts, existing home sales, NAHB home builders' index), are highlights of the economic calendar. The October producer price index will also be closely watched after the CPI report showed some moderation in inflation.

Regardless of which direction the market goes in, below we highlight one stock likely to be in demand and another that could see further downside.

Remember, though, our time frame is just for the upcoming week.

Stock To Buy: Chevron

I expect Chevron (NYSE:CVX) to enjoy a strong performance in the coming week, with shares likely to break out to fresh all-time highs, as investors continue to pile into the booming energy space amid the current environment.

CVX stock, which has outperformed the broader market by a wide margin this year, rose to $187.10 on Friday before closing at $186.46, above the prior record-high close of $185.61 from Nov. 7.

Year to date, shares have surged a whopping 58.9%, blowing past the gains made by competitors Shell (NYSE:SHEL) (+28.5%), and BP (NYSE:BP) (+27.1%) over the same time frame.

At current levels, Chevron has a market cap of $360.5 billion, making it the world’s second-most-valuable energy company, trailing only Exxon Mobil (NYSE:XOM).

Source: Investing.com

Energy stocks have enjoyed a blockbuster year as oil and gas prices remain elevated due to tighter global supplies following Russia's invasion of Ukraine earlier this year.

In fact, the Energy Select Sector SPDR Fund (NYSE:XLE) - which tracks a market-cap-weighted index of U.S. energy companies in the S&P 500 - is up 67.8%, making energy the top-performing sector of 2022.

In a sign of how well its business has performed in the current environment, Chevron delivered another period of explosive profit and sales growth when it reported Q3 financial results late last month, driven by improving global demand and rising production from its U.S. oilfields.

The energy giant posted a net profit of $11.2 billion, or $5.66 per share - almost double the $6.1 billion it recorded in the same period last year, and well ahead of the consensus $4.83 estimate.

Underlining its financial strength, Chevron’s cash flow from operations soared to a record $15.3 billion in Q3, much higher than in the preceding quarter.

Source: Investing.com

The company’s output from the U.S. Permian basin increased 12% from last year to top 700,000 barrels of oil equivalent per day (boed), reaching a quarterly record. Chevron reiterated its goal of pumping 1 million boed in the Permian in 2025.

As a result, I believe shares of the San Ramon, Calif.-based oil giant are well worth adding to your portfolio as they should see further upside in the days ahead.

Stock To Dump: Target

I anticipate Target's (NYSE:TGT) stock will suffer a difficult week ahead as the struggling big-box retailer’s latest financial results are likely to reveal a sharp slowdown in profit and sales growth due to the challenging macro backdrop.

Target is scheduled to deliver Q3 numbers ahead of the opening bell on Wednesday, Nov. 16.

Market players expect a big swing in TGT shares following the results, according to the options market, with a possible implied move of about 9% in either direction.

Source: InvestingPro

Consensus estimates call for the Minneapolis, Minn.-based retailer to report earnings per share of $2.18, down 28% from the year-ago period, amid the negative impact of rising operating expenses and higher freight and transportation costs on its business.

An Investing.com survey of analyst earnings revisions points to mounting pessimism ahead of the report, with analysts having cut their EPS estimates 23 times in the past 90 days to reflect a drop of -26.9% from their initial expectations.

Meanwhile, revenue is forecast to rise just 2.9% year over year to $26.4 billion amid numerous headwinds, including lingering inflationary pressures, rising interest rates, concerns about a slowing economy, and ongoing inventory and supply chain issues.

Taking that into account, I believe there is downside risk that management could cut guidance for the key fourth quarter - which covers the holiday shopping season - to reflect higher cost pressures and decreasing operating margins as the company cuts prices in an ongoing effort to clear unsold inventory from its shelves.

Source: Investing.com

TGT ended Friday’s session at $173.32, earning the retail giant a valuation of $79.7 billion.

Shares, which have bounced off their recent lows along with the major stock indexes, are down 25.1% year to date and are approximately 36% below their all-time high of $268.98 reached in November 2021.

Disclosure: At the time of writing, Jesse is long on the Dow Jones Industrial Average and the S&P 500 via the SPDR Dow ETF (NYSE:DIA) and the SPDR S&P 500 ETF (ASX:SPY). He is also long on the XLE (NYSE:XLE).

The views discussed in this article are solely the opinion of the author and should not be taken as investment advice.