- Six Flags' latest earnings weak compared to peers

- Share price has dropped

- Situation offers intriguing investment opportunity

Amusement park operator Six Flags (NYSE:SIX) is not performing well at the moment. The company’s second-quarter earnings were soft, while other theme park companies posted blowout results.

Looking forward, there are concerns about the broader economic environment and, of course, inflation. It seems little surprise that SIX stock declined 18% last Thursday, or that shares are down 45% from where they traded at the beginning of 2020.

Source: Investing.com

But there’s actually an intriguing investment opportunity here — precisely because Six Flags is not performing well. Management is acutely aware of the problems, and has an aggressive strategy to fix them.

It’s that strategy that has helped lead the stock to recapture nearly all of its post-earnings losses. And it’s that strategy that suggests SIX should have more upside from here.

Q2 Earnings Disappoint

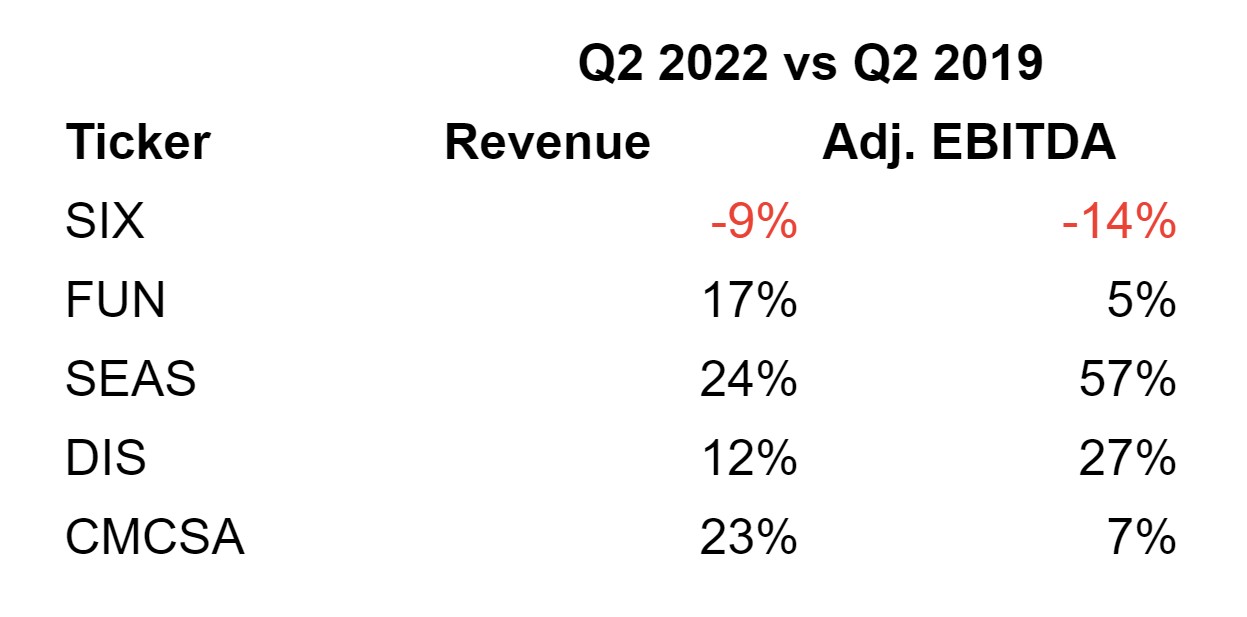

Six Flags earnings for the second quarter badly missed analyst estimates. But the bigger concern is how the company fared relative to other theme park operators:

Source: author

Pure-play theme park operators Cedar Fair (NYSE:FUN) and SeaWorld Entertainment (NYSE:SEAS) both delivered results well in excess of pre-pandemic levels. So did the theme park segments for diversified giants Disney (NYSE:DIS) and Comcast (NASDAQ:CMCSA).

Six Flags, however, has seen both revenue and profits decline on a three-year basis. That seems a huge concern with macroeconomic and inflationary risks looming.

SIX Stock Is Cheap

To at least some extent, SIX stock is pricing in the relative weakness of its performance. Based on trailing 12-month results, SIX trades at about 9x EV/EBITDA (enterprise value to earnings before interest, taxes, depreciation and amortization). That compares with a multiple of more than 13x before the pandemic.

On the same basis, FUN, probably the best peer, trades just shy of 10x. SEAS is at 8x, but that company is reliant on its Orlando-area attractions. That’s a risk to earnings both from a feared recession going forward and from a reversion to the mean following several quarters of insanely high travel demand. The businesses of Disney and Comcast’s parks generally have merited double-digit EBITDA multiples in sum-of-the-parts analyses.

So if Six Flags can get its performance fixed — and that’s a big if — there’s room for the multiple here to expand back toward pre-pandemic levels.

Absolute valuation works as well. Six Flags’ free cash flow averaged $285 million from 2017 to 2019; the current market cap of $2 billion-plus suggests a 7.5x multiple to that average.

In other words, to at least some extent the market is pricing in continued underperformance. And so, particularly given the leverage on the balance sheet, there’s a clear path to upside if Six Flags can change the trend.

The “Premiumization” Strategy

There’s a case the company can do so, because the existing problems seem to be self-inflicted. Before the pandemic, Six Flags aggressively pushed customers to a monthly membership plan for park access, even setting up kiosks at front gates to push the product. The company took a similar tack with concessions, launching an unlimited dining pass.

For a while, the strategy worked. But even before the pandemic hit, financial performance began to weaken. The focus on monthly subscriptions led to overcrowded parks, and long food-service lines. TikTokers literally figured out how to game the Six Flags dining pass, leading the company to abandon the plan earlier this year as part of its “premiumization strategy.”

That’s not the only change. Six Flags has ceased selling monthly memberships. It’s changing loading strategies to prevent empty seats on roller-coasters, while there is a 45-minute line of waiting customers. Free customers at one point accounted for about 10% of total attendance, yet as management has noted, those customers did not spend enough in-park to offset their impact on lines for dining and rides.

Changes are on the way. Maybe not all of these initiatives will work immediately, or necessarily at all — but there’s clearly a lot of low-hanging fruit here that can improve the park experience and hopefully financial results.

'Indefensible' Earnings

First-quarter results seemed to show some early progress on that front. Revenue increased 8% against Q1 2019. Attendance declined 22% over the same period, but per-person admissions spend rose 54% and in-park spending 58%.

On the call, CEO Selim Bassoul seemed optimistic that the strategy of lower attendance and higher revenue was working, though he did ask one analyst for “a few quarters” of patience.

Q2 earnings, however, were far more disappointing. Not only were results weaker than Q2 2019, but Six Flags posted declines on both lines (revenue -5%, EBITDA -9%) relative to the year-prior period.

As noted above, other theme park operators — who themselves are executing similar strategies — posted far stronger results. And so one analyst called Six Flags’ second quarter “indefensible.”

Keybanc raised the question of whether the attendance decline, in fact, suggests Six Flags’ pricing power is far less than management believes. The tone of the question-and-answer period on the second-quarter earnings call suggests that many other analysts have similar concerns.

But management said it simply overshot in its effort to lower attendance. The company wanted attendance to decline 20-25% from past highs, with the resulting better experience leading the remaining customers to pay more. Instead, attendance dropped roughly 35%.

That decline can and likely will be fixed. It will take time for Six Flags to communicate the improvements to its operations, the lower attendance and shorter lines, and perhaps the fact that the parks no longer are, as Bassoul put it on the earnings call, “cheap day care center[s] for teenagers.” One attendance miss, however large, in a single quarter doesn’t destroy the longer-term case for improvement.

And what seems attractive here is that valuation is reasonable now. If results improve as management believes, SIX stock will post significant upside. In fact, if management targets are hit, the stock roughly triples.

That upside is not guaranteed, obviously, but it highlights how the risk/reward seems heavily skewed in the bulls’ favor, even after the recent bounce.

Read the full version of this article at Overlooked Alpha.

Disclaimer: As of this writing, Vince Martin is long shares of Six Flags.