Larsen & Toubro (L&T) has lagged behind Nifty and MSCI India by 6% and 11%, respectively, and has underperformed its key industrial peers by over 30% year-to-date. According to Jefferies, this underperformance stems from lower operating leverage compared to its peers and disappointing guidance.

However, L&T is poised to surprise with its revenue guidance and has significant potential for order flow growth as the year progresses. Shareholder-friendly initiatives, including buybacks and higher dividends, are additional positives. The recent price correction has already factored in negatives, setting the stage for a 20% upside driven by improved return on equity (ROE) and growth.

Offer: By combining sophistication with flexibility, InvestingPro empowers investors to unlock hidden investment opportunities and navigate the complexities of the stock market with confidence. Click here to try it out for a limited-time 69% discount!

L&T's FY24 prospect pipeline saw a 14% year-over-year increase, achieving a remarkable 31% YoY order flow growth. Jefferies raised its FY25E order flow forecast by 5% following this strong performance. L&T's order book increased by 19% YoY, and the company achieved 26% YoY consolidated engineering and construction (E&C) revenue growth. For FY25E, Jefferies predicts an 18% YoY sales growth, slightly higher than the company's guidance.

The hydrocarbon and energy segment's order book rose to 25% from 18% YoY, with margins improving to 10% in FY24 compared to 6% in infrastructure. This segment's shorter gestation period is expected to contribute to margin stabilization and a 20-30 basis point uptick in FY25E. In FY24, hydrocarbons accounted for 16% of consolidated E&C sales, while infrastructure represented 71%.

L&T's ROE increased by 210 basis points in FY24 and is expected to rise by another 280 basis points to 17% in FY25E. The company conducted a Rs100 billion buyback (2.2% of share capital) and increased its dividend payout to 38% from 33% YoY. Jefferies believes continued improvements in ROE and cash flow will enhance shareholder value and lead to higher valuation multiples.

L&T's core E&C business is currently trading 43% below its previous upcycle peak in terms of EV/EBITDA. With strong capital expenditure momentum in India and the Middle East, Jefferies values L&T at Rs3,970, representing an 18x EV/EBITDA for September 2026E. For FY24-27E, Jefferies anticipates a 23% compound annual growth rate (CAGR) in core E&C EBITDA, compared to 16% in FY15-19 when it traded at 12x EV/EBITDA.

Jefferies highlights risks including imprudent capital allocation and a potential reduction in government infrastructure spending. Despite these risks, L&T stands to benefit from the revival of the capex cycle, with significant improvements in ROCE and ROE since the FY16 bottom.

Image Source: InvestingPro+

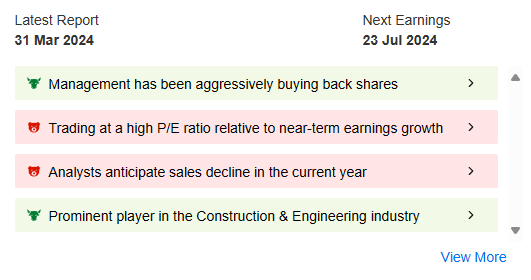

Also, investors should forget about the valuations of a company no matter how good of a growth trajectory is. ProTips makes it easy for investors to find any red flag in the company that might not come on investors’ radar. In this case, it highlights valuation concerns - High P/E relative to near-term growth. It also says that analysts expect sales decline this year which could negatively impact the share price.

Now, how to know about the true worth of the stock? The simplest answer is the fair value. After analyzing this counter from 9 financial models, the average intrinsic value (fair value) comes at INR 2,961, meaning the stock is overvalued by 13.6%. This is an important metric to gauge whether it would be fruitful to buy this counter or not.

InvestingPro, the ultimate stock analysis tool, is now within reach at a discount of up to 69%, offering unparalleled insights for just INR 216 per month, but hurry, this offer won't last long! Click here to grab it today!

Read More: Unlocking Investment Potential via Fair Value

X (formerly, Twitter) - Aayush Khanna